Stack

Mobile Application | Figma | Prototype | UI/UX Research

Overview

Stack is an AI-powered finance app that is built for the next generation. With a personalized AI assistant, it helps young adults take control of their money, build better habits, and grow up as financially fearless adults in an AI-first world.

My Role

UX Research and Product Designer

Duration

1 month

Interact with Prototype

Introduction

The Value of Managing your Money

Money is a tool for value exchange - it governs the existence of every being on this planet. Your resources, your opportunities and your autonomy are shaped by it.

The brain's reward circuits are shaped early in life - the habits we form around money - saving, spending and deferring instant gratification - become hardwired patterns. Practicing money management from a young age is, therefore, not just practical, it is crucial to building lives of clarity and sustainable freedom.

All systems tend towards entropy without intentionally defined structures - unmanaged finances are no exception to this law.

Living in an AI-first World

Just as money shapes the architecture of our choices, Artificial Intelligence (AI) will radically shape the architecture of our consciousness.

The way I see it, AI reflects our collective database of knowledge as humans. To ignore it or fear it, is to deny our own evolution. Exposure to intelligent systems, will sharpen our cognitive flexibility and help us navigate complex environments more efficiently, as long as we engage with it consciously and with a deep desire to evolve with it. On the flip side, outsourcing our minds to machine poses darker implications for us as humans, but that's another conversation.

Guiding young minds to interact meaningfully with AI is not about replacing human insight, but augmenting it with more knowledge to make data-informed decisions, even if you're not an expert in data and numbers. It enables a generation that is not just financially literate, but conscious about it's evolving future.

Key Problems

What are the issues young adults seem to face

when navigating money?

Lack of Financial Literacy

Without understanding basic financial concepts like budgeting, compound interest, credit, taxes, or debt - young adults are set up to make poor decisions, often unknowingly.

Debt Mismanagement

Carrying high-interest debt without a repayment plan can cripple financial mobility and mental health.

Financial Anxiety or Avoidance

When finances feel overwhelming or shame-inducing, people often freeze or ignore them entirely.

Impulsive Spending

The dopamine-driven behavior of impulsive purchases and instant gratification (especially due to quick e-commerce shopping) can drain savings and fuel debt.

Lack of Goal-Oriented Budgeting

Without clear financial goals (short- and long-term), budgets feel restrictive instead of empowering.

Peer Pressure and Lifestyle Inflation

Trying to keep up with peers can lead to spending beyond one’s means as income grows.

Poor Saving Habits

Not saving early means missing out on compound growth and facing future emergencies unprepared.

Inconsistent Income Streams

Freelancers and gig workers often have unpredictable cash flow, making budgeting harder.

Tools That Speak Their Language

Traditional finance tools are boring and complex. They aren't personalized enough for younger audiences.

Solution Space

Design a user - friendly, mobile interface that unifies different functions of money management actions.

Intelligent, Adaptive Financial Literacy AI

Assistant

A dynamic AI assistant that answers all your money-related queries based on your personal finances. It also teaches financial concepts in curated bite-sized, personalized modules.

Real-Time Spending Guidance & Smart Automation

AI-powered nudges that track spending behavior in real time and offer context-sensitive advice (e.g. "You’re close to overspending on dining this week. Want to auto-move funds to savings instead?").

Goal-Based Budgeting & Visualization Tools

A highly visual interface that allows users to create short- and long-term financial goals (e.g., travel, emergency fund, debt payoff) with interactive progress tracking.

The Process

A visual flow of the steps we will follow, to create a user-focused finance management product.

Discover

Define

Develop

Deliver

Insight into problem

Scope down focus

Potential Solutions

Solutions that work and receive feedback

Fig 1: A Double Diamond Model of Approach

Phase 1: Discover

To gain deep and thorough insights on the defined problem space.

User Research

1. Primary Research:

(Quantitative Online Survey)

We created an online survey to understand if real user data supported the established problem and solution space, that called for the need of an AI-driven financial management tool for young adults. It would also help us better understand what features would define the scope of our initial minimum viable product.

The survey was blindly sent to 100s of people with 20 responses gathered.

1.1 Primary Research:

(Quantitative Online Survey Results)

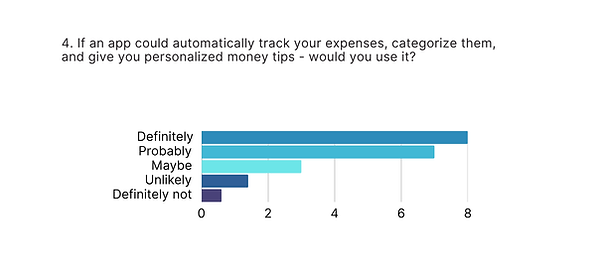

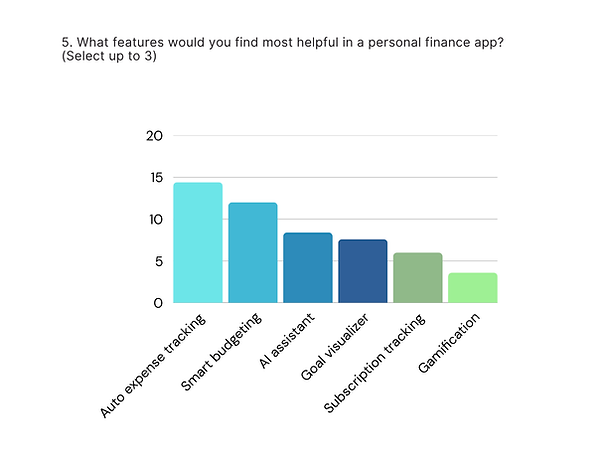

The data collected from the survey of 20 people, are visualized below for better understanding. Key insights were drawn from the data that would assist us in defining the scope of our MVP.

QUICK INSIGHT

Most GenZ users are relying on basic tools like notes or spreadsheets, revealing a gap in smarter, automated systems.

QUICK INSIGHT

Expense visibility and impulsive spending dominate GenZ money struggles.

QUICK INSIGHT

75% are open or excited to use AI for finance - a strong opportunity for adoption.

QUICK INSIGHT

75%+ of users show interest in using an AI finance assistant, if it’s trustworthy and helpful.

QUICK INSIGHT

Core features should focus on automation and simplicity over gimmicks.

1.2 Primary Research:

Key Insights from the Online Surveys

Our quantitative survey targeting Gen Z participants revealed a clear gap in current personal finance habits and tools.

Over 70% of respondents admitted to feeling overwhelmed or inconsistent when tracking their spending, while 65% lacked a structured savings habit. A significant portion- over 60% - expressed interest in automated, personalized financial advice to help them budget better and reach goals faster.

These insights validate the core hypothesis behind Stack: young adults crave smart, intuitive tools that simplify money management. The demand for an AI-powered assistant that can guide, remind, and empower them financially.

2. Primary Research:

(Qualitative Interviews with 5 people)

In-person/organic interviews offer deeper, more emotionally rich insights that digital surveys often miss. Human decision-making, especially around money, is driven less by logic and more by emotions, habits, and identity. By observing body language, tone, hesitation, and non-verbal cues, qualitative interviews tap into subconscious attitudes and internalized beliefs about finance.

For a Gen Z audience navigating anxiety, aspiration, and financial independence, these conversations reveal not just what users do, but why they do it. This context is invaluable for designing an empathetic, behaviorally aware AI tool.

2.1 Primary Research:

(Affinity Mapping the Results)

Affinity mapping is a method that will help us synthesize and derive insights of the qualitative information collected. By clustering similar sentiments and pain points, it's a way of noticing underlying behavioral and thought patterns that shape our target audience's mind and behavior with respect to money management. Raw unstructured data was grouped into broad themes to make sure that the app's features translated into what the users deeply craved without being able to fully articulate it.

“I get low-key stressed just opening my bank app.”

“Makes me feel like I'm managing it inefficiently ”

“I avoid checking balances unless I HAVE to.”

EMOTIONAL PATTERNS

Money seems to be tied to a lot of anxiety and fear, due to lack of proper management.

“I just check my transaction history on GPay… I don’t really track it.”

“I use Notes to write down monthly expenses, but I forget to update it, after a week and give up.”

"I've tried using apps before, but they're so dull and complex"

LACK OF SYSTEMS

Almost none of them tracked their finances in a systemic way. Knew their methods were inefficient, but had inertia in adopting complex tools.

“I downloaded Mint once and deleted it in a week.”

“Too many charts, and options, not very intuitive for beginners.”

"I'm not really sure how to start budgeting and dividing my resources optimally, when I'm on the app. There's zero guidance or feedback"

COMPLEXITY OF APPS

Most of them found finance management apps daunting and not intuitive. They didn't find any reason to engage with it due to lack of understanding and knowledge on how to budget correctly.

“I want to travel more, maybe invest, but I don’t know how to start.”

"I want to learn how to save and invest in stock markets but I'm not sure where to begin."

“Saving feels impossible with rent and impulsive spends"

INTERESTED IN SAVING AND INVESTING

All of them expressed a desire to save and invest, and knew the importance of it for their future. But all of them felt like they lacked the knowledge on how to budget their finances and couldn't do it without external guidance.

“If it worked like a chatbot and gave me real tips based on my actual finances, I’d use it.”

“I want something that just tells me what to do based on my habits and income."

"That sounds really interesting and useful. I would definitely feel more confident letting AI setup structures and budgeting plans for me. "

HIGHLY RECEPTIVE TO EXPLORING AFINANCE AI-ASSISTANT

All of them expressed interest, sometimes very strongly in allowing AI to analyze their transactions and help them break down their budgets and push them to achieve their savings goals.

2.2 Primary Research:

Key Insights from the Personal Interviews

-

There’s a very strong emotional gap between GenZ’s money habits and their desired financial behavioral states.

-

Many don’t want data visualization and manual tracking - they needed empathetic guidance, personalized feedback, automation, and simplicity.

-

There’s a very strongly expressed, opportunity for an AI finance tool that feels friendly, conversational, and adaptive to their individual lifestyles.

3. Competitor Analysis

This matrix compares top personal finance tools across key feature categories that matter to our target audience. The goal is to understand what differentiates Stack from other apps and if there's a demand for another finance management app on the market.

There is a definite demand for an AI-powered finance assistant for which there is a definite deficit in the current finance management tools available on the market.

%20(1).jpg)

3.1 Competitor Analysis: Key Takeways

-

Stack stands out with a built-in AI assistant, Gen Z–friendly gamified savings, and AI-powered personalized insights.

-

Apps like YNAB are powerful but might feel outdated or too complex for Gen Z users who are just beginning to track their finances.

-

Fi Money is closest in positioning but lacks the level of personalization and conversational guidance offered by Stack.

Phase 2: Define

To define the scope of the problem, based on the user research conducted.

Target Audience

4. Defining the Target Users

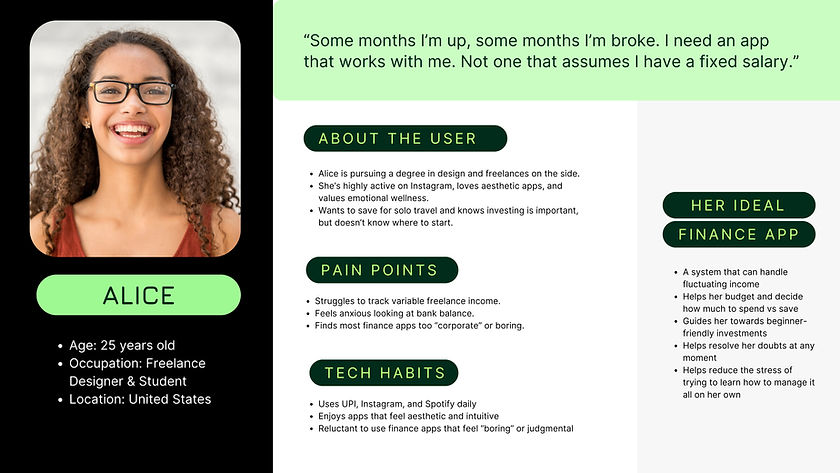

Our target audience will consist of young adults (commonly referred to as GenZ) of the ages 18-30, who are in the initial stages of building their wealth and forming systems to manage it. They are recent graduates and early professionals. They’re digital natives - comfortable with technology, highly active on mobile, and expecting intuitive, aesthetically pleasing, and emotionally intelligent experiences from the apps they use.

.jpg)

User Personas

5. Understanding our Users

User personas are fictional representations of our key user types built from patterns observed in our previous qualitative and quantitative research. We attempt to distill complex human behavior into fictional profiles to ensure we are always empathizing and designing for our users.

There are infinite gradients of humans, but complex psychological frameworks pioneered by psychologists like Carl Jung (MBTI), allow us to predict and deeply map out human behavioral patterns according to their most commonly used cognitive functions. While we won't attempt to derive that here to limit the scope of our case study, we will attempt to define two broad categories of humans that illustrate our most common users.

5.1 Empathy Mapping our Users

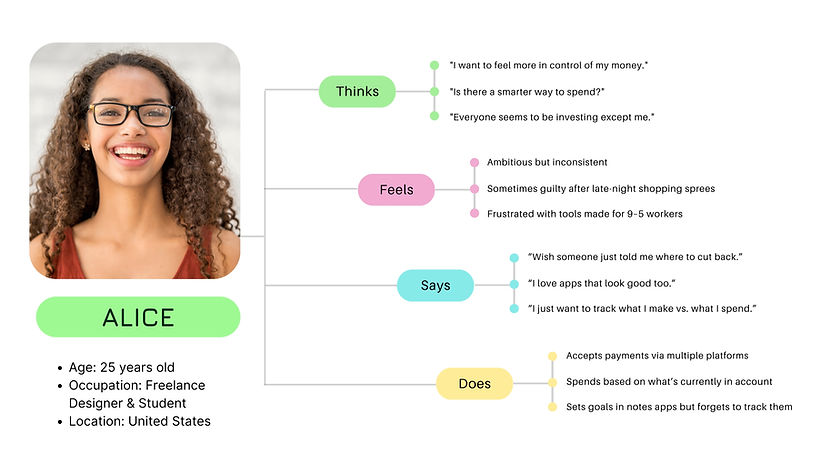

Empathy mapping is a crucial step in human-centered design, allowing teams to deeply understand users beyond surface-level behaviors. By visualizing what users think, feel, say, and do, empathy maps further dig into hidden motivations, emotional drivers, and unmet needs.

6. User Journey Mapping

User personas defined the general user archetypes and empathy mapping tries to undertsand the internal mindset of the user. User journey mapping shows how these users behave over time within the defined system. To design an intelligent user flow, it's important to map out the whole journey of the potential user. Since, we've already tried to deeply grasp their mindsets and behaviors we will now attempt to define how they might interact with out application prototype to understand how to maximize the value they derive.

.jpg)

Phase 3: Develop

To brainstorm and develop the MVP, based on all user research conducted.

Brainstorming Features

7. Tasks/Features Matrix

We will attempt to exhaustively define all the possible features that will need to be developed, in order to estimate the time and resources that will be required to build out and deliver the initial MVP.

The features will be categorized into:

1. Core MVP Features (These are crucial to the initial product and will form the first iteration)

2. Nice-to-Have Features (These are features that are valuable, but not essential to first launch and test)

3. Future enhancements (These are advanced/experimental features for later stages of the product)

MVP (Minimum Viable Product) – Launch First

These are must-have features that address Gen Z’s most immediate pain points like lack of financial clarity, overspending, and inconsistent tracking. They deliver immediate value and help differentiate Stack from other apps through AI-powered assistance.

AI Finance Assistant

Answers financial questions, gives personalized advice, helps with app navigation

Add Expenses/Income

A large add button, to add all your recent spends/income

Expense Tracking

Real-time categorization of income and expenses

Budgeting Tool

Tool that helps you set a monthly budget and automatically calculates your remaining spend.

Upcoming Bill Tracking

Track, manage and pay bills and subscriptions from one unified screen

Spend Analyzer

Visual breakdown of spending behavior with weekly insights

Smart Notifications

Nudges for bill reminders, overspending alerts, budget limits

Basic Gamification

Fun savings streaks or milestone tasks to build financial discipline

Basic Profile Settings

Manage your account details, including connecting your bank/cards/UPI

Nice-to-Have Features (Post-MVP)

These add depth, retention, and social engagement. Build once we have a core user base.

Subscription Management

Track, manage, and cancel digital subscriptions from one place

Expense Splitting

Easily split bills and payments with friends or roommates

Personalized Finance Tips

Daily bite-sized finance tips from Lumo

In-app Rewards

Visual rewards for reaching savings goals or streaks

Multi-currency Support

Useful for travelers and students studying abroad

Future Enhancements – Experimental & Growth Features

Build later as the app matures, user data grows, and we identify deeper needs.

Voice-Activated Commands

"Hey Stack, what's my budget for food this week?"

Financial Health Score

AI-generated credit-style score based on habits

AI-Driven Expense Forecasting

Predictive budgeting to pre-empt overspending

Integration with Wearables

Push financial nudges via smartwatches

8. Prioritization Matrix of Features

This matrix maps features according to User Impact (High / Low) vs Feature Priority (High / Low). It helps with product planning discussions.

Priority vs Impact Matrix

High Priority

High Impact

Low Priority

Low Impact

Add Expenses/Income

Expense Tracking

Budgeting Tool

Upcoming Bills

Spend Analyzer

Smart Notifications

Basic Gamification

Profile Settings

Bank Linking

AI Finance Assistant

Subscription Mgmt.

Expense Splitting

Personalized Tips

In-App Rewards

Multi-currency support

Voice commands

Finance Health Score

Wearable Integration

AI Expense Forecast

Information Architecture

9. Defining the User Flow

A well-defined Infomration Architecture helps organize the app's structure into a flow of screens that is most logical and intuitive for the users. It provides product stakeholders, developers and designers with a unified framework that aligns everyone around a shared vision of the product and helps them define the technical scope and timeline of the product more quickly.

.jpg)

Wireframes

10. Lo-fidelity wireframes

To ensure alignment with stakeholders and user needs, we start out with quick lo-fidelity wireframes as the first iteration of our MVP. This helps surface any flaws in scope, layout and user navigation early on in the project before we start building complex design systems to host the higher fidelity mockups.

.jpg)

Phase 4: Deliver

To design and iterate on user feedback

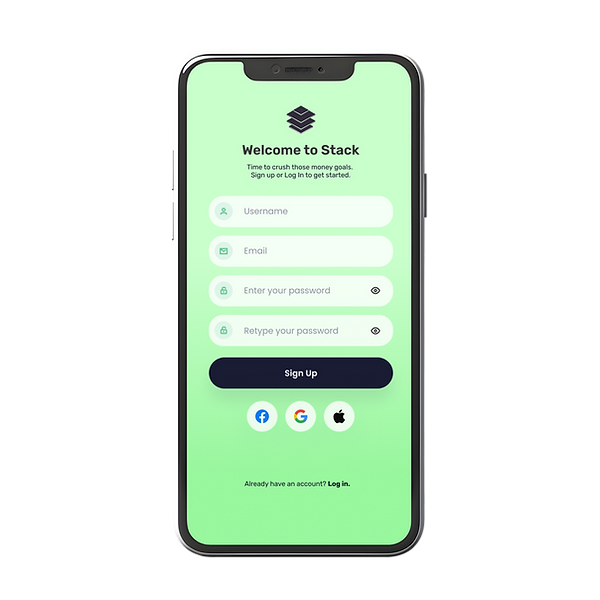

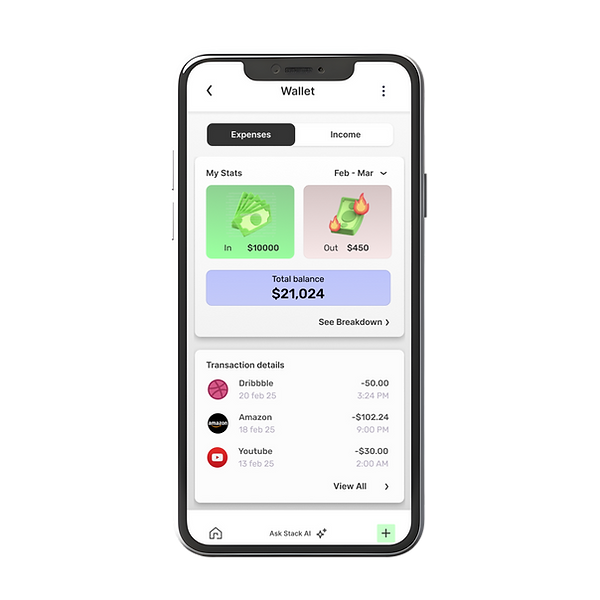

11. Hi-fidelity mockups and prototype

The final product prototype was designed on Figma using the Material Design 3 Design System for quick, cohesive implementation.

Login/Signup Screens

Home Screen

Wallet

Budget

Payments

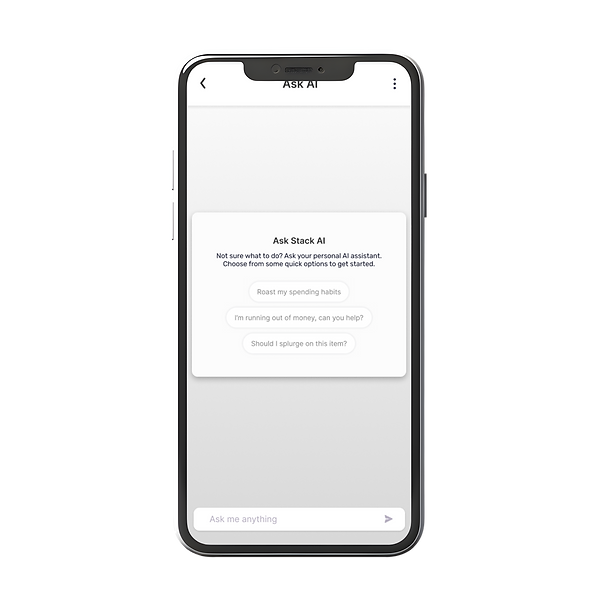

Ask AI Screens

Add Expenses